Deloitte’s fourth “Global Automotive Supplier Study” analyzes shareholder value performance for more than 200 automotive suppliers. The study posits that the change in the face of mobility will be driven by disruptive trends such as connected and autonomous technology, shared mobility and electrification. Most importantly, these changes will likely force industry players to rethink strategies to drive superior shareholder value creation in the future.

The Shifting Value Equation

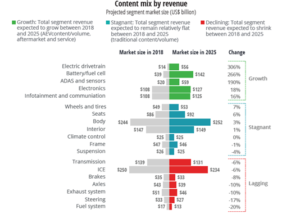

According to CapIQ, in 2018 the total combined revenue of the global automotive supplier market was $1.7 trillion. Deloitte’s segment analysis estimates that some segments could face as much as 20% in revenue erosion over the next five to seven years, while some higher-growth segments could more than triple their current revenues.

Suppliers driving innovation in autonomous and electrified systems will likely see the most opportunity and growth (as much as approximately 300% in some segments), while those operating in more commoditized automotive supply segments like frames, interiors, brakes and internal combustion engines could be at risk as these segments stagnate and decline between now and 2025.

“Industry players have operated in an automotive market filled with uncertainty throughout the past decade, and with the future of mobility in full throttle massive changes are still expected,” said Neal Ganguli, managing director, Deloitte Consulting LLP, and U.S. automotive supplier practice leader. “Suppliers and industry participants must recognize that past or current success is not an indicator for the future. These companies must analyze their portfolios and outlook to develop strategies to help them create superior shareholder value, regardless of the future their business portfolios face.”

Growing, Stagnant And Declining Product Segments Face Different Futures

Segments with the strongest growth potential and ability to differentiate will be the most attractive, according to Deloitte. These include advanced driver-assistance systems; infotainment and communication; batteries and fuel cells and electronics and electric drivetrains. Suppliers in these segments might consider expanding by developing and acquiring cutting-edge technologies, defending their position by acquiring competitors to increase base and maintain growth in shareholder value or pivoting by spinning off growth businesses to focus strategic priorities and resources.

Segments that are more stagnant can seek cost leadership and pathways to innovation and growth through offering intelligent, customized solutions over and above just the systems hardware, such as customized, private and configurable interiors and personalized climate zones. Suppliers might expand by shifting R&D and capital investments toward growth segments, while driving; defend by acquiring or merging with peers; or pivot by divesting business units and products that do not contribute to a long-term strategic direction.

Suppliers in declining segments have already started using scale to harvest profits and maximize cash flow through the product decline life cycle. These suppliers might expand by investing in developing markets with less technological investment; defend by harvesting remaining shareholder value within lagging business by consolidating and leveraging scale; or pivot by selling struggling business to competitors or private equity buyers.

Winds Of Change

Four mega-trends — shared mobility, electrification, technology convergence and new market entrants — are driving disruption in the automotive industry. While each of these forces has already begun impacting the industry, it is the convergence of these forces, in combination with looming macroeconomic headwinds that will likely cause a dramatic shift in the way automotive suppliers across the value chain compete and reshape the automotive value chain.

Overall, now is not the time for industry leaders to sit idly. Instead, industry executives should think through their business portfolio, including which businesses they should harvest or divest, which ones they should fix, and which ones they should fund for growth.

For more information on Deloitte’s “2019 Global Automotive Supplier Study,” or to download a copy, please visit: http://www.deloitte.com/us/autosuppliers.