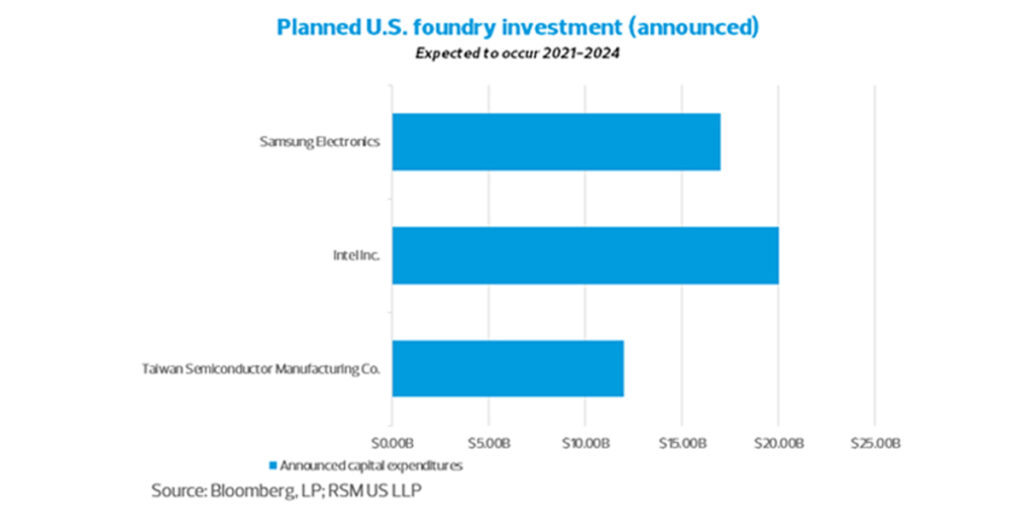

In response to significant order backlog and surging demand for microchips, global semiconductor manufacturers are looking to expand existing plant capacity in the short term while also taking steps to open new foundries—also known as fabs—to handle anticipated long-term demand growth. The world’s current leading chip manufacturers Taiwan Semiconductor Manufacturing Co. and Samsung Electronics, along with Intel, have announced capital expenditures for such plans, which will direct billions of dollars to the American Southwest over the next few years; this investment will kick-start the U.S. reentry into the space and raise the global chip production ceiling.

The supply crunch is the result of a range of factors, some related to the pandemic. Foundry shutdowns aimed at curbing the spread of COVID-19 last year contributed to a reduction in chip supply just before global demand for consumer electronics, gaming consoles, automobiles and other products requiring such chips soared. In recent months, semiconductor supply chain disruptions have stalled production of the Ford F-150 at two U.S. plants, reduced the supply of next-gen gaming consoles such as Xbox Series X and PlayStation 5, delayed the launch of game company Intellivision’s highly anticipated Amico console by almost a year, and sent shocks through other sectors as well.

But this is not only a recent issue; the United States “has outsourced and offshored too much semiconductor manufacturing in recent decades,” according to a recent White House review of the nation’s supply chains, which found that “the United States has fallen from 37% of global semiconductor production to just 12% over the last 20 years.” This loss of capacity “threatens all segments of the semiconductor supply chain as well as our long-term economic competitiveness.”

U.S. expansion plans from TSMC, Samsung and Intel represent future growth opportunities for middle market players in semiconductor manufacturing-adjacent industries as manufacturers move to ramp up production to meet this booming demand.

A Well-Suited U.S. Hub

The water-reliant microchip manufacturing process is largely responsible for drawing global attention to the drought in Taiwan, where TSMC has four foundries. This process also makes the famously dry American Southwest a less-than-intuitive locale for multibillion-dollar investments to manufacture such chips. But there is already an established semiconductor manufacturing ecosystem in Arizona; the state has emerged as a U.S. “manufacturing hotspot” in the push to “insulate semiconductor supply from China,” Fortune reported in February.

During an interview with CNBC, Forrester Research vice president Glenn O’Donnell compared semiconductor manufacturing to an indoor swimming pool: “You need a lot [of water] to fill it, but you don’t have to add much to keep it going. Also, being in an enclosed space, a lot of the water that evaporates can be captured with a dehumidifier and returned to the pool.” This comment suggests that water availability may not be an ongoing burden to the manufacturing process once volume production commences.

Also crucial for making semiconductors is access to affordable, stable energy. In Taiwan, the cost of electricity is at risk of increasing by as much as 25% by 2025, according to Bloomberg, which reports: “the government’s rigid denuclearization policy and emission reduction targets imply that more-expensive renewable electricity will be the only choice for manufacturers’ surging energy needs.” In Arizona, semiconductor manufacturers will have access to the U.S. power grid as well as renewable energy sources including solar.

Sourcing Talent

With record demand and billion-dollar facilities on the horizon, companies will need to be strategic about recruiting a capable workforce. Talent in the field is tough to find, but not as tough in the Southwest as it would probably be in many other parts of the United States. Arizona has an established, yet largely dormant, semiconductor manufacturing ecosystem and also an active semiconductor design market, both of which are anticipated to streamline the U.S.’s imminent march back into chip manufacturing.

Phoenix has long been the unofficial microelectronic manufacturing hub of the United States, and Andy Blye of the Phoenix Business Journal reports: “Phoenix is home to many other semiconductor companies as well. NXP, ON Semiconductor, Microchip and Broadcom all have employees here.” Companies in the process of establishing (or reestablishing) fabs in the American Southwest will likely source expertise necessary to run the highly anticipated foundries by either relocating talent or by drawing from the established semiconductor design workforce that already exists in cities such as Phoenix. Middle market semiconductor companies, or those adjacent to this space, would likely see waves of hiring by TSMC, Intel and Samsung, which could lure talent away or push wages higher.

Additionally, the chip shortage has spurred political action, as this June blog post on the Semiconductor Industry Association’s website explains: “Bipartisan legislation introduced this week in the House would eliminate the counterproductive per-country cap on employment-based visas in favor of a fair, ‘first come, first served’ system, providing U.S. semiconductor companies with greater access to top talent from around the world needed to compete and innovate.”

Future Possibilities

It’s important to remember that the rush for capable employees is still a ways off; TSMC’s wafer fabrication plant in Phoenix “is expected to start volume production in 2024,” according to Reuters, and “Intel expects the Arizona fabs to be operational sometime in 2023,” Morningbrew.com reported in May. TSMC has committed $12 billion for a foundry in Phoenix, with “construction slated to start next year.” And in May, Reuters reported that TSMC may build up to five fabs in Arizona.

Although volume production manufacturing appears to be a few years away, manufacturing-adjacent industries can be expected to gear up, creating new opportunities for the American middle market. Mainly, semiconductor equipment companies and suppliers, packaging companies and testing shops should prepare for a wave of change over the next few years. This is a great time for these companies to determine how they will adapt to the reintroduction of large-scale volume production; shore up relationships with their own workforces, contractors and existing supply chains; and set aside capital to allow for strategic agility.

The strategy to build resilient semiconductor supply chains for the future “must include taking defensive actions to protect our technological advantages,” according to the White House’s supply chain review. “But we must also proactively invest in domestic production and R&D.”

With approved capital expenditure plans, experienced workforces to tap, potential eases forthcoming for employment-based visas, and an ever-growing demand for chips, the future appears bright for semiconductor manufacturing in the United States. However, the trickle-down effects of reemerging domestic chip production are still in large part many years away from having significant impact on the global chip market and the middle market.

This article originally published via RSM US LLP, the national’s leading provider of audit, tax and consulting services focused on the middle market. It was authored by Nate Farshchi, Director and Technology, Media and Telecommunications Senior Analyst and Davis Nordell, Senior Manager, Technology, Media and Telecommunications Senior with RSM.