Automotive manufacturers and suppliers continue to face pandemic-provoked challenges including production shutdowns, an accelerated shift to virtual sales, and parts shortages. Deloitte’s fifth “Global Automotive Supplier Study” examines the trends influencing significant structural changes across virtually every arm of a heavily nuanced and complex global automotive supply chain. The report is based on quantitative analysis of shareholder value performance from nearly 300 of the top global automotive suppliers and interviews with senior automotive supplier executives.

Growth for new and legacy segments continues to accelerate

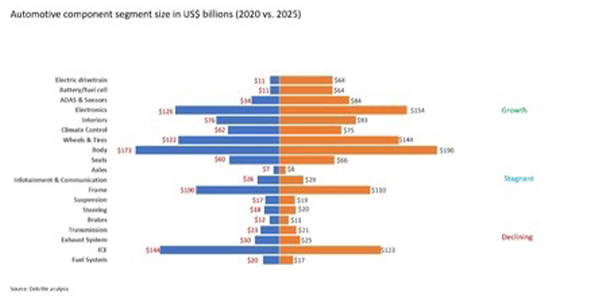

As the industry grapples with shifting priorities driven by the growth in electric vehicles (EVs), suppliers are refocusing their investments on technologies for the road ahead. Component clusters tied to the future of mobility, including advanced driver-assistance systems (ADAS) and electric propulsion, are positioned to see significant growth in market size through 2025.

Both electric drivetrains and battery/fuel cell segments are poised for exponential growth, each projected to increase 475% between 2020 and 2025, combining for a market size of $128 billion at the end of the forecast window.

Additional segments positioned for growth include ADAS and sensors (150%), electronics (22%) and interiors (21%).

Despite internal combustion engine (ICE) parts showing a 15% reduction by 2025, its market share forecast of $123 billion, along with vehicle frames ($110 billion), demonstrates these segments will remain highly relevant for suppliers looking to capitalize on consolidation opportunities in this space.

ICE and hybrid powertrains will comprise 85% of total global engine production in 2025, signaling robust demand for legacy propulsion technology to the middle of the decade.

“As we’ve seen in the last year and a half, material scarcity led to significant production challenges, and the semiconductor crisis could be a harbinger of things to come. A resulting material constraint would have a knock-on effect on an entire emerging segment that would keep prices high and further limit EV market penetration. To position their businesses for success, automotive suppliers need to make decisions now about whether to expend or defend their current positions, or pivot to something new. Further, by taking stock of where their raw materials are sourced and maintaining sufficient distribution strategies automotive suppliers can help avoid severe commodity restraints that could damage already strained automotive relationships,” said Raj Iyer, managing director, Deloitte Consulting LLP.

Potential roadblocks

The semiconductor crisis has illuminated not only an immediate supply chain vulnerability, but several critical issues that have been percolating just below the surface as the global industry readies for a future characterized by EV mobility.

In an effort to mitigate future chip shortages, auto manufacturers are looking to renegotiate for longer contracts and direct partnerships with chip suppliers. To combat one of the root issues that contributed to the lack of forecasting and supply chain visibilities, suppliers could consider retiring obsolete technologies. This involves updating ageing information technology systems and investing in greater data transparency to benefit the complex relationship between multiple tiers of parts suppliers and their vehicle manufacturer customers.

Further compounding the challenges among automotive suppliers is the war for talent. As the industry readies for a future driven by EV mobility, demand for software developers and data engineers to support this fundamental shift is at an all-time high. Meanwhile, the manufacturing sector is faced with a persistent skills gap and ongoing challenges posed by COVID-19 and its emergent variants.

The road ahead

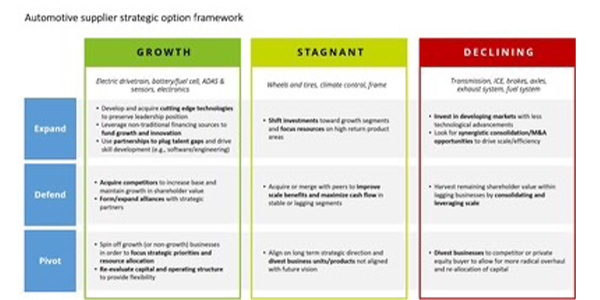

Both in the near and long term, suppliers should adequately prepare their organizations for a future that is rapidly approaching. Suppliers face the critical point in the industry roadmap where they need to expand or defend their current positions or pivot toward something new.

Through strategic consolidation, acquisitions and alliances, suppliers have the opportunity to better protect margins and diversify risk across growing, stagnant and declining supplier sectors. Managing related complexities among existing technologies and emerging trends will likely require swift decision-making to achieve short-term shareholder value and long-term success.

“As a result of the pandemic, automotive suppliers have learned how to operate leaner and should continue to remain flexible to shifting economical, geopolitical and logistical issues. Suppliers should make strides to shore up regional production pillars to minimize volatility around production uncertainty and dependence on costly expedited freight to meet near-term demands. Further, they must be flexible for a future that is arriving faster than expected. Of all the raw materials required to forge the next step in global automotive mobility, time is perhaps the scarcest,” SAID Jason Coffman, U.S. automotive consulting leader and principal, Deloitte Consulting LLP.

KEY TAKEAWAYS

- Electric vehicles (EVs) are poised for exponential growth, with the market size for parts tied to electric drivetrains as well as batteries and fuel cells expected to increase475% in the next five years, while legacy component clusters tied to fossil fuels will stagnate but remain relatively robust over the next several years.

- Ongoing supply concerns may extend to commodities necessary for the production of EV batteries, including lithium, cobalt and nickel.

- Through strategic consolidation, acquisitions and alliances, suppliers have opportunities to better protect margins and diversify riskacross growing, stagnant and declining supplier sectors.

Learn more at www.deloitte.com.